For payment service providers, digital wallets, and fintech platforms, transaction routing is no longer just an infrastructure decision. It is now a direct lever for margin protection, approval-rate improvement, and customer experience. In markets like Dubai, where payment ecosystems are highly connected and competition is intense, even small routing inefficiencies can create visible losses over time.

This is where AI least cost routing for payments is becoming strategically important. Instead of sending every transaction through fixed, rule-based paths, fintech teams can use intelligent systems that evaluate cost, approval probability, risk signals, issuer behavior, and acquirer performance in real time. The result is a smarter routing model that can reduce avoidable fees while supporting stronger authorization outcomes.

For PSPs and payment-led fintech businesses, the opportunity is clear. Autonomous AI agents can help build more adaptive payment operations, strengthen routing decisions across gateways and acquirers, and support a more scalable transaction stack.

Operational Challenge

Many PSPs still depend on routing logic built around static priorities. One acquirer may be set as default, another as backup, and a few manual rules may define what happens when a transaction fails. That approach worked when payment ecosystems were simpler, but it often breaks down in modern multi-provider environments.

The main challenges include:

1. Rising processing costs

Different acquirers, gateways, and payment methods come with different fee structures. If routing logic is not continuously optimized, PSPs can end up paying more than necessary on large transaction volumes.

2. Low approval rates from rigid routing

A fixed path may ignore issuer behavior, regional performance patterns, or payment-method-specific approval trends. That can lead to unnecessary declines and weaker conversion.

3. Complex multi-provider environments

Modern payment stacks often include multiple gateways, banks, fraud engines, payment orchestration layers, and settlement partners. Managing this manually becomes difficult at scale.

4. Slow reaction to performance changes

Acquirer reliability can change by hour, geography, card type, merchant category, or traffic spike. Static systems usually react too late.

5. Limited visibility into routing quality

Without strong analytics, teams may know their total costs and approval rates, but not which routing decisions are creating losses or friction.

This is why payment routing optimization AI is gaining attention in fintech. It helps organizations move from reactive routing to adaptive decision-making.

How the Solution Can Be Implemented

Implementing autonomous routing does not require replacing the entire payments stack at once. A more practical path is to build AI-driven intelligence around the existing routing and orchestration layer.

A typical implementation can follow this structure:

Step 1: Connect and Normalize Data Sources

The first step is to unify transaction data from gateways, acquirers, fraud tools, issuer response logs, retry flows, and chargeback systems. This creates the data foundation needed for routing intelligence.

In practice, this goes beyond simple API integration. Fintech systems must normalize different response codes, latency logs, settlement formats, and provider-specific data structures into a single, consistent, and queryable schema. Without this normalization, routing intelligence cannot function effectively at scale.

Step 2: Define routing objectives

The AI system should be trained and configured around business priorities such as:

- lowest processing cost

- highest approval likelihood

- best route by payment type or geography

- fraud-aware routing

- failover during provider disruption

In practice, most PSPs need a balance of cost, conversion, and risk rather than a single routing metric.

Step 3: Build decision agents

Autonomous agents can evaluate live conditions before a transaction is sent. These agents can check:

- current acquirer success rates

- issuer-specific decline patterns

- transaction value and payment method

- region or corridor performance

- risk score and fraud signals

- expected fee impact

This creates a more dynamic AI payment gateway routing model than rule-based systems alone.

Step 4: Introduce feedback loops

Every routing decision should feed back into the model. If one route becomes expensive, unstable, or decline-prone, the agent can adjust future decisions based on recent outcomes.

Step 5: Launch in controlled phases

A phased rollout is safer. Fintech teams can start with a limited merchant segment, a single geography, or specific transaction types. Once performance becomes measurable, the system can expand across the broader payment network.

This phased model is often the most practical way to answer the question of how AI reduces payment processing costs in PSPs without creating operational risk.

Functional Components

A strong autonomous routing setup usually includes several business-critical capabilities.

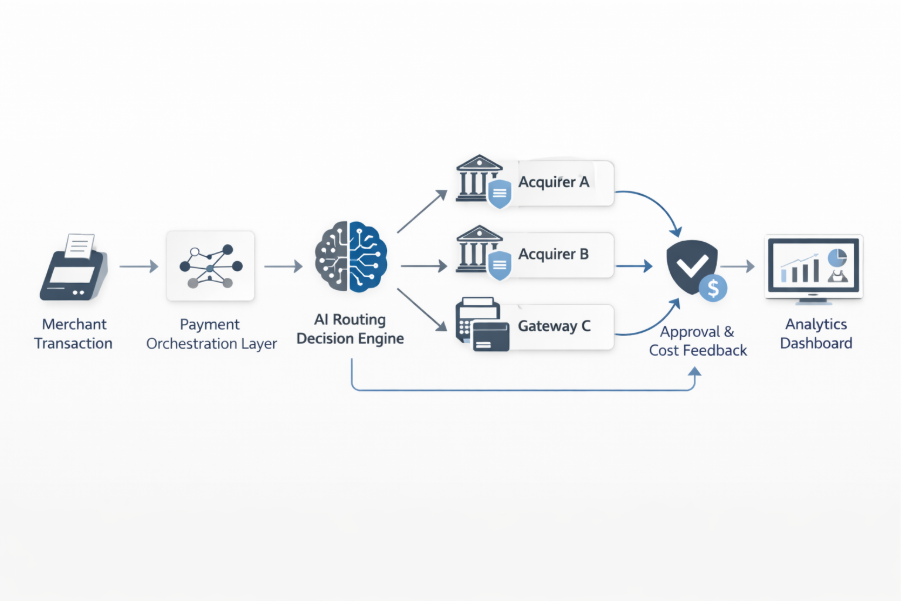

Fig. Workflow of an AI-driven payment routing engine showing the transition from orchestration to real-time acquirer selection and the continuous feedback loop for cost and approval optimization.

Real-time route scoring

The platform can evaluate each possible route using cost, approval probability, latency, and risk. This is the core of intelligent payment routing systems.

Multi-acquirer decision logic

A routing engine should support switching between acquirers based on issuer history, payment method, geography, and merchant context. This enables a smarter multi-acquirer routing strategy.

Performance-aware failover

If one gateway or acquirer underperforms, the system can shift traffic without waiting for manual intervention.

Fraud-aware routing decisions

Transactions with elevated risk may require a different route, additional checks, or stricter approval logic. This is where an AI fraud and risk routing engine adds value.

Continuous learning

Over time, the system can detect new approval trends, cost anomalies, or routing inefficiencies and refine its logic.

Analytics and routing dashboards

Decision-makers need visibility into cost per route, approval changes, issuer response patterns, retry success, and routing impact by segment.

Technology Stack

A successful routing architecture needs more than a model. It needs a practical workflow that fits PSP operations and compliance requirements.

A common architecture may include:

- transaction ingestion layer from gateways and payment processors

- data pipeline for normalizing issuer, acquirer, and fraud signals

- routing intelligence engine using rules plus machine learning

- orchestration layer that applies route decisions in real time

- monitoring dashboards for finance, operations, and product teams

- audit logs for compliance and explainability

For PSPs building dynamic transaction routing fintech systems, cloud-native architecture is often the most flexible option. APIs connect payment gateways, fraud platforms, merchant systems, and analytics services. Event-driven workflows can help evaluate live traffic without slowing down transaction speed.

This is also where custom fintech web application solutions can play an important role. A dedicated internal dashboard can help operations teams monitor routing quality, finance teams analyze cost performance, and product managers test routing scenarios. Well-designed custom fintech web application solutions can make complex routing decisions more visible and actionable for business users, not just engineering teams.

At the platform level, many fintech companies combine payment orchestration tools, decision engines, model-serving infrastructure, and cloud observability layers. This makes payment orchestration platforms a strong fit for AI-led routing execution.

Commercial Impact

When implemented correctly, autonomous routing can create measurable commercial value.

Lower processing costs

The clearest benefit is cost control. Better route selection can help reduce avoidable fees across high-volume traffic. In some PSP environments, routing improvements can support cost reductions in the range of 10 to 30 percent, depending on the provider mix and current inefficiencies.

Better approval rates

AI-driven route selection can improve authorization performance by sending transactions to providers with better issuer alignment or higher success probability.

Faster response to network conditions

Instead of waiting for manual escalation, the system can adapt when provider performance shifts.

Stronger merchant experience

Higher approvals and fewer failed retries improve checkout continuity for merchants and their customers.

Better operational insight

Routing dashboards can reveal which combinations of gateway, issuer, acquirer, and region are creating waste or friction.

This is why many fintech teams are now exploring least cost routing fintech solutions as both a cost strategy and a conversion strategy.

Adoption Considerations

In payments, optimization cannot come at the expense of control. Any AI-led routing model should be built with governance in mind.

Key considerations include:

Explainability

Operations and compliance teams should understand why certain routes are selected, especially when routing affects cost, approvals, or risk treatment.

Data security

Transaction data must be protected with strong encryption, access controls, and secure cloud infrastructure.

Regulatory alignment

PSPs operating in the UAE and cross-border markets should align routing architecture with relevant payment compliance, data governance, and audit requirements. For PSPs operating in the UAE, this may also require alignment with Central Bank of the UAE (CBUAE) payment regulations, along with internal audit controls, model governance, and transaction-level transparency requirements.

Human oversight

Autonomous systems should not be unmanaged systems. Teams need override controls, monitoring thresholds, and approval workflows for major routing changes.

Model drift monitoring

Issuer patterns, network performance, and fraud behavior change over time. Models should be reviewed and recalibrated regularly.

A practical least cost routing strategy for digital payments UAE should always balance automation with trust, transparency, and operational control.

Real-World Example

Consider a Dubai-based cross-border marketplace PSP handling card payments for regional merchants across the UAE and GCC. The platform processes high volumes of international transactions and works with multiple acquirers and gateways to support global payment acceptance.

After introducing an AI-led routing layer, the PSP begins evaluating each transaction based on card type, issuer history, region, amount band, fraud score, and recent acquirer performance. Low-risk domestic payments may be sent through the most cost-efficient route. Cross-border payments with higher decline risk may be routed to the provider with stronger issuer acceptance. If one acquirer shows abnormal latency, traffic shifts automatically.

Over time, the PSP gains clearer insight into AI-based payment routing for high approval rates and identifies which provider combinations work best by use case. The result is a more resilient and commercially efficient payment operation.

Why This Matters

For CTOs, heads of payments, product leaders, and operations teams in Dubai fintech companies, routing is now a strategic capability. The region’s payment landscape is growing quickly, and businesses need infrastructure that can handle more complexity without creating more overhead.

Autonomous routing matters because it supports three outcomes at once:

- cost discipline

- higher approval performance

- scalable payment operations

For PSPs in particular, this is not just a technical upgrade. It can shape merchant retention, transaction margins, and platform competitiveness. In a market where payment efficiency affects both revenue and trust, smarter routing becomes a meaningful differentiator.

What This Means for Key Decision-Makers:

For CFOs: Better visibility into processing costs and reduced fee leakage across high-volume transactions.

For Heads of Payments: Improved control over approval rates and routing efficiency across multiple providers.

For Product Teams: The ability to enhance payment performance without rebuilding the entire payment infrastructure.

Frequently Asked Questions

1. What is AI least cost routing for payments?

It is an AI-driven approach that selects the most cost-efficient transaction route while also considering approval probability, risk, and provider performance. It improves on static routing by making decisions in real time.

2. How is payment routing optimization AI different from traditional rule-based routing?

Traditional routing uses fixed rules and limited fallback logic. AI-based routing can analyze live data, learn from outcomes, and adjust routes based on changing issuer, gateway, and acquirer conditions.

3. Can AI payment gateway routing improve approval rates as well as reduce costs?

Yes. A strong routing model can balance both objectives. It can choose routes that are more likely to succeed while still controlling processing fees and reducing inefficient retries.

4. Is autonomous routing suitable for small or mid-sized fintech companies?

Yes, especially if they work with multiple gateways or acquirers. A phased rollout can start with limited traffic segments and expand as the routing model proves value.

5. What data is needed to implement intelligent payment routing systems?

Useful inputs include transaction history, issuer responses, approval and decline patterns, gateway latency, acquirer fees, fraud scores, retry performance, and payment method behavior.

6. Are there compliance concerns when using AI for payment routing?

Yes. PSPs need secure data handling, audit logs, explainable routing logic, and governance controls. Human oversight remains important even when decisions are automated.

7. What is the first step in adopting least cost routing fintech solutions?

The first step is usually data unification. Once transaction, cost, and performance data are connected, teams can begin testing routing models and rollout strategies with far better control.

Conclusion

Autonomous AI agents can help PSPs move beyond static routing and toward a more adaptive payment strategy. By combining cost awareness, approval optimization, risk signals, and live provider performance, fintech teams can build routing systems that are more efficient, more scalable, and easier to improve over time.

For payment businesses in the UAE, this implementation path is especially relevant. Competition is strong, transaction diversity is growing, and margins depend on smarter decision-making. A well-designed routing architecture, supported by internal dashboards, orchestration logic, and clear governance, can create measurable gains without forcing a full platform rebuild.

For companies exploring AI fintech development services Dubai, the strongest opportunity lies in building practical, controlled, and insight-driven systems that improve both cost efficiency and transaction outcomes.

Move beyond basic failovers

Looking to design a smarter payment routing system for your PSP or fintech platform?

Theta Technolabs helps businesses build AI-powered fintech products with strong expertise across Web, Mobile, and Cloud solutions. From routing intelligence dashboards to orchestration-ready platform components, the team can support scalable implementation aligned with business and compliance needs.

To discuss your use case, reach out at sales@thetatechnolabs.com and explore how a practical AI routing strategy can support lower costs, stronger approvals, and better payment operations.

Meta Description -

Learn how AI payment routing improves approval rates, lowers costs, and builds smarter fintech payment systems for PSPs and digital platforms.

.avif)

.avif)

.avif)

_How%20IoT%20Can%20Reduce%20Energy%20Costs%20in%20Smart%20Factories_Q4_25.avif)

_How%20AI%20Development%20Companies%20in%20Ahmedabad%20are%20Transforming%20the%20Shopping%20Experience_Q4_25.avif)

_Node.js%20and%20Blockchain_%20A%20Perfect%20Pair%20for%20Fintech%20Innovation%20in%20Dubai_Q3_24.avif)

_Choosing%20the%20Right%20Computer%20Vision%20Development%20Partner%20in%20Ahmedabad%20for%20Construction_Q3_24.avif)

_The%20Transformative%20Role%20of%20Open%20Banking%20APIs%20in%20Fintech%20for%202024_Q3_24.avif)

_Explore%20the%20Best%20Cross-Platform%20App%20Development%20Frameworks%20of%202024_Q3_24.avif)

_Integrating%20IoT%20with%20Mobile%20Apps%20for%20Advanced%20Renewable%20Energy%20Solutions_Q2_24.avif)

_Top%20Benefits%20of%20Cloud%20Computing%20for%20All%20Business%20Sectors_Q2_24.avif)

_Understanding%20the%20Impact%20of%20AI%20and%20Machine%20Learning%20on%20Fintech%20Web%20Apps%20in%20Dubai_Q2_24.avif)

_Smart%20Manufacturing%20in%20Dubai_%20How%20AI%20is%20Driving%20Efficiency%20and%20Innovation_Q1_In_24.avif)

_Automated%20Checkout%20Systems.avif)

_Smart%20Solutions%20for%20Healthcare_%20How%20IoT%20Development%20is%20Reshaping%20Dubai%20Hospitals_Q1_In_24.avif)

_Computer%20Vision-enabled%20Web%20and%20Mobile%20Interfaces%20for%20Mall%20Management%20in%20Dubai_Q1_In_24.avif)